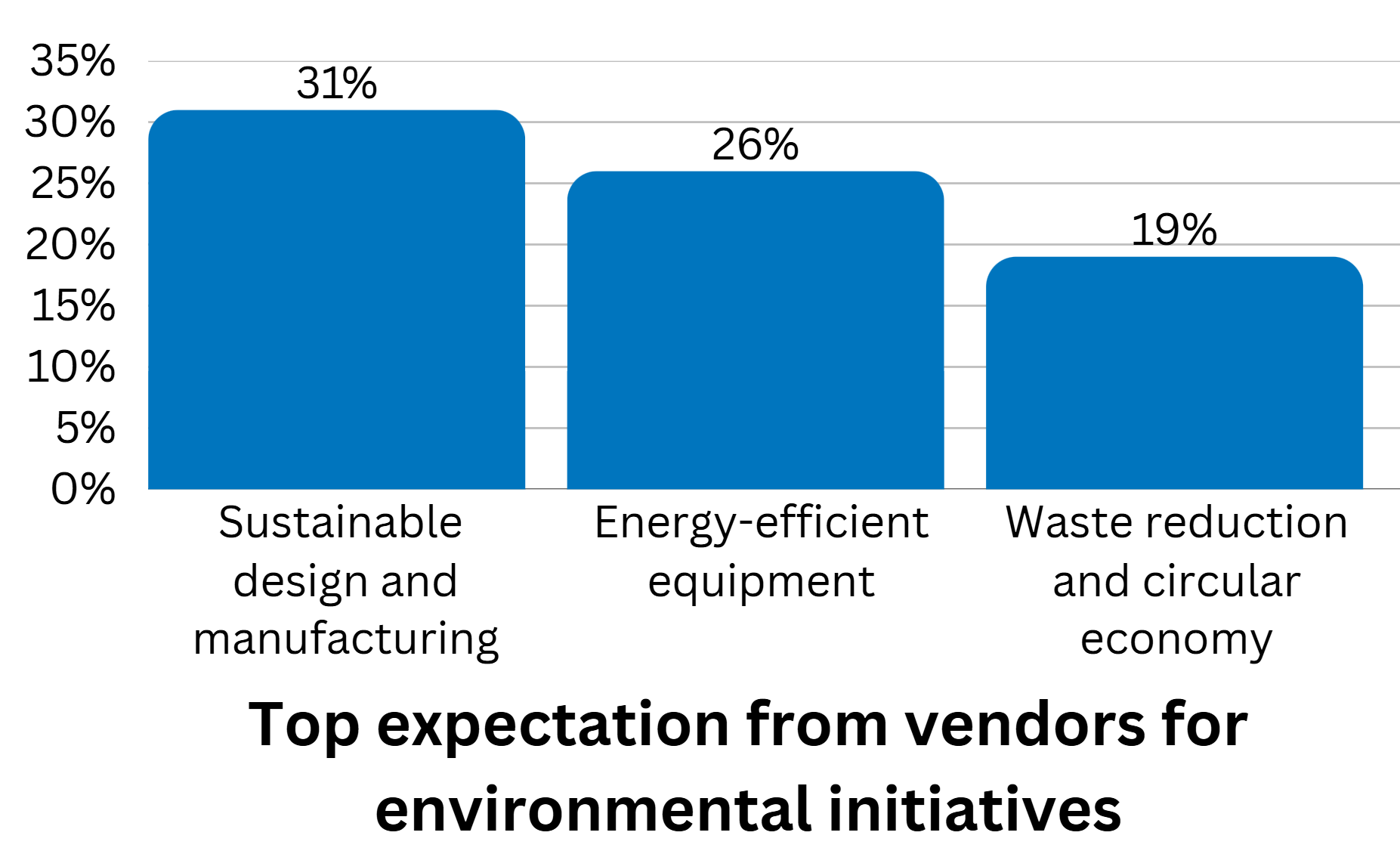

The top expectations are for vendors to offer sustainable design and manufacturing of equipment (31% of imagePRO panel members), energy-efficient equipment development (26%), and to reduce waste and improve circular economy (19%).

IVD Market Intelligence Q4 2025

March 17, 2026

Share this article:

By James Garvin, Senior Consultant at The Marketech Group | March 2026 | Estimated read time: 8 minutes

Three Forces Reshaping Clinical Diagnostics in Q4 2025

The Q4 2025 earnings cycle marked a strategic reset for the global in vitro diagnostics (IVD) industry. Two major transactions reshaped the competitive landscape: TPG’s acquisition of Hologic and Water’s purchase of the diagnostics division from BD. These moves signal a broader realignment across the sector as companies sharpen their focus on higher-growth segments and reposition portfolios for the next phase of diagnostics innovation.

At the same time, three structural forces are redefining how value is created in the industry. China’s procurement reforms are compressing margins across core testing markets, growth is shifting toward high-value specialty assays rather than new instrument placements, and a rapidly intensifying race in rapid antimicrobial susceptibility testing (AST) is reshaping the microbiology competitive landscape.

An analysis of eleven leading diagnostics companies’ Q4 results reveals how these forces are beginning to separate strategic winners from laggards heading into 2026.

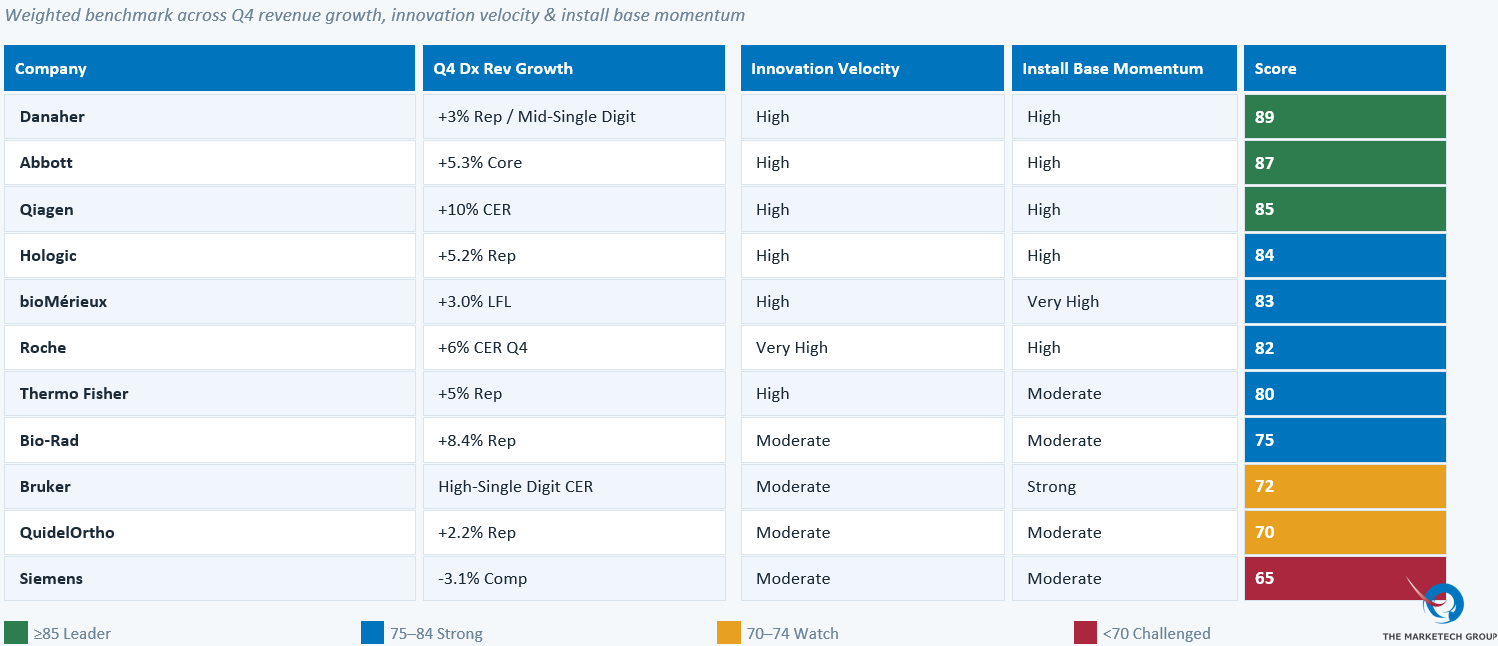

To better understand how the industry’s leading players are navigating this transition, we created a Q4 2025 IVD Performance Scorecard evaluating eleven major diagnostics companies across three strategic dimensions: revenue momentum, innovation velocity, and installed base strength. The scorecard combines publicly reported earnings data with qualitative indicators such as platform expansion, assay menu growth, and competitive positioning to highlight which companies are building durable competitive advantage in the evolving diagnostics market.

Part 1: The Three Forces Reshaping the IVD Market

After three years of pandemic-driven volatility, the IVD market has found its footing again, but it looks different than 2019. Growth in Q4 2025 is anchored by routine hospital testing, chronic disease monitoring, and a now-predictable respiratory baseline. The windfall of COVID diagnostic demand is gone, replaced by something more durable: steady volume in immunology, oncology, transplant monitoring, and chronic disease panels.

Specialty diagnostics — oncology companion diagnostics, neurodegenerative disease markers, transplant monitoring — are outperforming general diagnostics across nearly every platform reviewed. For commercial teams, this means the messaging shift from "reliability and throughput" to "clinical utility and patient pathway value" is not aspirational — it is already underway in the field.

The single most consequential structural factor in Q4 2025 IVD results is China's Volume-Based Procurement (VBP) policies. The scale of impact is striking:

- Roche Diagnostics reported an absolute annual revenue headwind of approximately $666 million USD (CHF 579 million) from China VBP pricing reforms. Excluding China, global diagnostics grew +7%.

- Abbott Laboratories quantified a $400 to $500 million annual China VBP headwind. Core Lab Diagnostics achieved three consecutive quarters of acceleration (+5.3% reported in Q4).

- Combined, these two companies alone are absorbing a ~$1.1 billion annual revenue gap from a single market.

The implications for IVD commercial strategy are direct: companies under this margin pressure must urgently recoup profitability in the United States and Europe through premium novel assays, expanded menus, and higher-value testing categories.

Primary Research Question

What is the maximum price premium US and EMEA lab directors are willing to absorb for novel, high-value assays — before test volumes begin to decline?

During the pandemic, the IVD industry competed on platform placement — getting instruments into labs, clinics, and hospitals at scale. That wave has crested.

In Q4 2025, the competitive battleground has definitively shifted from instrument placements to assay menu expansion. Capital equipment budgets are constrained. Laboratories resist buying new boxes. QuidelOrtho's Labs business grew +7% in Q4, with instrument revenue flat and growth driven entirely by consumable pull-through — a pattern repeated across the industry.

Simultaneously, clinical mass spectrometry automation is creating an entirely new regulated IVD category. This is a ~$3.45 billion USD market currently served primarily by manual laboratory-developed tests (LDTs). Roche (cobas i 601), Thermo Fisher, and others are pushing to bring automated, regulated alternatives to market.

Part 2: Segment-by-Segment — Where the Growth Is

Roche Diagnostics achieved the most dramatic sequential turnaround — from flat in Q3 to +6% CER in Q4, with +10% growth in Core Lab excluding China. The forthcoming cobas i 601 Mass Spec (CE marked) automating therapeutic drug monitoring and vitamin D testing represents their most significant platform innovation for a US launch in 2026. The Elecsys pTau217 and NfL assays position Roche squarely in the high-value Alzheimer's and neurology diagnostics category.

Abbott Laboratories is executing one of the most consequential M&A moves in IVD in years: the pending acquisition of Exact Sciences will add a high-growth cancer screening vertical to Abbott's traditional immunoassay and chemistry base. Three consecutive quarters of Core Lab acceleration provide the financial runway to pursue this integration

.

Danaher (Beckman Coulter) achieved six consecutive quarters of mid-single-digit or better Core Lab growth, with immunoassay growing at high-single-digit rates. The DXi9000 expansion into cardiac, blood virus, and neurodegenerative disease markers is the platform differentiation bet for 2026.

Siemens Healthineers represents the most significant strategic watch in Core Lab. With Q4 Diagnostics revenue down -3.1%, the company has "verticalized" its Diagnostics division to run independently — language management tied explicitly to evaluating "all strategic optionality." With Atellica now driving 70% of core lab revenue in the Americas, competitive displacement research is urgently needed.

Danaher (Cepheid) reported that core non-respiratory test menu grew low double-digits, with sexual health testing up +30% in Q4. A newly FDA-cleared GI Multiplex PCR panel is in global rollout. The 2026 outlook centers on approximately $1.8B in respiratory revenue alongside a growing non-respiratory base.

Hologic announced it is being taken private by TPG in an $18 billion transaction leveraging its now 3,400+ global Panther installed base newer high-throughput vaginitis testing (BV/CV/TV). Hologic’s management noted the company is "only in the middle innings of realizing the total opportunity." Molecular Diagnostics grew +6.7% reported (+11% excluding COVID).

bioMérieux's SPOTFIRE platform is the single most explosive growth story in molecular diagnostics this quarter: +84% revenue growth in Q4, 6,400 total units installed globally, with approximately 900 new units in Q4 alone and reagent sales up +56%.

Qiagen delivered +10% CER diagnostic growth, with QIAstat-Dx expected to scale from $109M (FY2024) to approximately $130M (FY2025). QuantiFERON delivered +14% CER in Q4, yet 60% of the latent TB testing market still uses traditional skin tests — a massive unconverted opportunity.

Thermo Fisher achieved FDA 510(k) clearance for Exens — the first fully automated platform for multiple myeloma diagnosis — alongside an FDA-cleared NSCLC companion diagnostic. An NVIDIA AI partnership for lab automation and diagnostic decision support is underway.

Bio-Rad is achieving something genuinely novel: the migration of digital PCR (ddPCR) from Research Use Only (RUO) to regulated IVD, with the QX600 platform becoming the first digital PCR system to make this transition. Two strategic IVD partnerships (Gencurix and Biodesix) anchor the commercial expansion strategy.

Part 3: The BD Diagnostics Exit — The Decade's Biggest Displacement Opportunity

The most consequential competitive event in IVD market structure in Q4 2025 is Becton Dickinson's divestiture of its Diagnostics segment to Waters Corporation, completed at an estimated $3.5 billion.

BD Diagnostics reported pre-exit Q4 revenues down -9.6%, with the Rapid Diagnostics segment declining -17.8% as COVID antigen test volumes continued their post-pandemic normalization. Full-year Diagnostics revenue is estimated at approximately $4.2 billion.

Waters Corporation (NYSE: WAT), historically a scientific instruments and HPLC/mass spectrometry vendor, has made its largest-ever acquisition and its first entry into regulated clinical diagnostics. This creates what we assess as one of the largest competitive displacement opportunities in IVD in a decade:

- Customers face legitimate uncertainty about long-term menu innovation, support commitments, and R&D investment under Waters

- The primary beneficiaries in Core Lab and Microbiology are bioMérieux, Roche, Danaher (Beckman Coulter), and Abbott

- In Rapid Diagnostics and POC, QuidelOrtho and Abbott POC are best positioned to absorb displaced customers

Part 4: The 2026 IVD Research Agenda — 14 Questions Requiring Primary VOC Data

These fourteen research questions represent the most commercially consequential unknowns facing diagnostics companies heading into 2026; questions that cannot be answered only through secondary data alone.

| | Segment | Research Question |

|---|---|---|

| 1 | Market · Pricing | What is the maximum price premium US and EMEA lab directors will absorb for novel assays before test volumes decline? |

| 2 | Market · Capital | How are hospital lab directors prioritizing capital investment for analyzer consolidation vs. adding new specialized assays? |

| 3 | Core Lab · Mass Spec | What are the primary workflow pain points for current manual LDT Mass Spec users that will drive adoption of automated IVD alternatives? |

| 4 | Core Lab · Oncology | How do health system oncology stakeholders prefer to engage with Core Lab vendors when evaluating high-value cancer diagnostics? |

| 5 | Core Lab · Displacement | What are the core displacement triggers that would cause a lab director to switch from Roche or Abbott to the Siemens Atellica platform? |

| 6 | Core Lab · Immunoassay | How much weight do lab directors place on extreme immunoassay sensitivity versus pure menu breadth when selecting a new core lab platform? |

| 7 | Molecular · Multiplex | What clinical utility arguments are most effective in convincing clinics to adopt multiplex GI or STI testing on an existing respiratory platform? |

| 8 | Molecular · Women's Health | What are the primary remaining barriers to OB/GYN clinics adopting high-throughput molecular vaginitis testing? |

| 9 | Molecular · TB | What are the primary economic and clinical hurdles preventing the remaining 60% of the latent TB market from converting to QuantiFERON? |

| 10 | Molecular · Genomics | What are the key buying criteria for clinical genomics labs when evaluating high-throughput sequencers vs. established Illumina platforms? |

| 11 | Microbiology · AMR | What health economic data is required to justify the premium ROI of rapid Gram-Negative blood culture testing to hospital administrators? |

| 12 | Microbiology · Displacement | How entrenched is bioMérieux's dominance, and what specific operational gaps must Bruker's Wave platform solve to win meaningful market share? |

| 13 | Specialty · Myeloma | What does the current sample journey look like for multiple myeloma patients, and where does automated IVD offer the greatest time-to-diagnosis value? |

| 14 | Specialty · ddPCR | What regulatory-grade workflow features are most critical to convincing clinical labs to adopt ddPCR over established PCR platforms? |

Conclusion: The Intelligence Gap Is Strategic

The in vitro diagnostics industry enters 2026 with three of its largest players managing China-driven revenue headwinds, the most significant ownership transition in its Core Lab segment in a decade, and a post-pandemic recalibration that has fundamentally shifted where competitive advantage is built.

The companies that will capture disproportionate share in this environment are not those with the most comprehensive earnings analysis. They are those that understand — at the level of specific clinical stakeholders, specific workflows, and specific purchasing triggers — what lab directors actually want, and what will make them act.

Work with The Marketech Group

The Marketech Group is a MedTech marketing research consultancy specializing in the IVD and medical technology industries. We design and execute primary research that translates market signals into actionable marketing & commercial intelligence.

Our 2026 IVD research capabilities include:

- Global VOC Studies — Structured interviews and surveys with lab directors, clinical scientists, and procurement leaders across US, EMEA, and APAC

- Pricing Research — Conjoint analysis, willingness-to-pay, and price elasticity studies for novel assay and platform launches

- Platform Displacement Research — Identifying the specific triggers that cause lab directors to switch platforms

- Sample Journey & Workflow Mapping — Ethnographic research into clinical diagnostic workflows to identify unmet needs

- Concept & Messaging Optimization — Pre-launch testing of clinical claims and value propositions with target buyer segments

- Competitive Wargaming — Structured research-based competitive positioning studies for platform launch strategy

If your team is evaluating a platform launch, menu expansion, or competitive displacement strategy in 2026, these questions are not theoretical — they are commercial decisions.

The Marketech Group designs VOC research to answer them before launch.

The Marketech Group publishes quarterly IVD Market Intelligence Reports synthesizing earnings data from the industry's leading diagnostic companies. This analysis covers Q4 2025 results reported in January–February 2026.

2025 MICI Q4 Shows S mall Increase in Overall Confidence from Q3 2025

Discover how ESG is reshaping healthcare—from sustainable imaging and energy‑efficient design to equity and governance strategies driving industry transformation.

2025 MICI Q3 Shows Less Confidence in Reimbursement and Capital Access